A Focus on Coins in the Cash Cycle

Without coins you cannot receive change when you pay with a banknote. Although banknotes receive most attention in the cash cycle, April’s MDC webinar reminded people why that is a mistake.

Kathleen Young, Senior Vice President of FedCash Business Operations for the Federal Reserve System’s Cash Product Office (CPO), and Jim Douthitt, Head of Treasury at Coinstar, gave two different viewpoints of coins in the US in the last 12 months. David Hensley, from Enryo consulting, added a UK perspective.

Coinstar’s perspective

Jim started by explaining that the US has an unusually large proportion of its population who rely on cash for payments. 6.5% of households are unbanked and 18.7% underbanked, together 32.6 million American households. These households are significant users of Coinstar’s coin services.

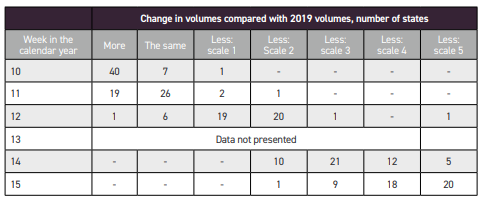

A series of maps showed how coin return volumes changed across 48 American states as the pandemic spread.

In pre-pandemic times US banks deposit $3.4 billion with the Federal Reserve, from non-Coinstar sources. A further $2 billion are deposited through banks from Coinstar. Add in Mint production of $0.9 billion and the Federal Reserve received $6.3 billion coins, allowing it to fulfil coin orders.

The Federal Reserve would normally receive $1.35 billion worth of coins each quarter. However, in the pre-pandemic quarter ending 15 June 2021 only $0.52 billion of coins were returned, a 61.5% reduction. Coinstar would usually receive $0.5 billion, but received $0.24 billion in that quarter, a 52% reduction.

Coinstar believes its high number of cash dependent users account for its higher rate of return. Another contributory factor is that its equipment is located in retailers and, as essential services, they did not close. In contrast, many bank branches did.

The ratio of orders to deposits stabilised by the end of 2020. The gap is now normal, although coin returns remain about 25% lower than pre-pandemic. Getting coins moving remains a challenge.

Coinstar gave three lessons learned from the past year:

If the cash system only works if the volumes are at a given level, then it is highly vulnerable if, and when, a segment of the population goes cashless.

The cash cycle needs to have higher levels of stock and greater storage capacity ready for when disruption happens.

There is an opportunity to improve localised transparency to allow better cash management.

Federal Reserve perspective

Coin in circulation has returned to growth and by the end of February 2021 had reached $48.4 billion. It is, however, growing more slowly than banknotes.

The effects of the pandemic were not immediately obvious as coin demand grew in line with normal levels ahead of the Spring holiday break. The first indication of a change was a drop in deposits. This was followed by a significant and continued increase in coin demand. This created a net payment gap that required the introduction at the start of July of a coin allocation system. This lasted through until the start of February 2021. More usual patterns of order and deposit are now returning, albeit still at lower levels than normal.

The coin allocation system was necessary because the US Mint could not produce new coins fast enough to fill the gap. The problem was not insufficient coins but coins not circulating. As a result, a major element of the response, alongside the creation of a Coin Taskforce to address supply challenges, was a public education campaign to get coins moving.

One of the lessons learned is that financial institutions are good at talking to retailers but not so good at reaching the public. As came out in the panel discussion, reaching the public proved a major challenge.

Who drives cash volumes?

In the webinar’s panel, the relative reliance, and use, of cash by different segments of society was a key part of the discussion.

David Hensley was one of the authors of the UK’s Access to Cash report and although the UK’s cash reliant segment is smaller than that of the US, it isn’t that much smaller. David’s consultancy, Enryo, have conducted five surveys into UK cash usage over the last year and those who are frequent users of cash have hardly changed their behaviour.

Ironically, therefore, circulation depends on people who use little cash. They are the ones who hold high levels of coins at home unused. Communicating with this group proved, and continues to prove, to be a real challenge.

Cash flow

For the coin, and cash, cycle to work, there needs to be a flow of coins around the system. In the UK there are about a million ‘places’ to spend cash (a taxi, for example, could be a ‘place’) and about 6 million tills. With costs under scrutiny, the cash cycle is fragile. There is about five days worth of stock in that system at any one time. The flow is huge, and it needs a lot of cash to be in the system for it to work efficiently. ‘We don’t really understand where the cash is’, stated David.

In the US, the response to the pandemic saw cash in circulation rise 20% as people fled to cash. $315 billion has been put into circulation during the pandemic and most of it is still out there.

One of the lessons learned, stated by both the Federal Reserve and Coinstar, is that bigger stocks need to be held as a protection against disruptive events. If coin return is the first casualty of a crisis, and you can’t mint your way out of a problem, then stock needs to be in the right place at the right level. If coins now start to return, the Federal Reserve could choose to use these to build those stocks.

Forecasting

The number of transactions at a high street level was seen as key to determining cash requirements rather than circulation levels.

David Hensley suggested Coinstar’s receipts are a reasonable proxy to measure this. The Federal Reserve develops a range of scenarios rather than trying to forecast precisely.

Rounding up prices

There was a discussion about the benefits of rounding up prices to reduce the number of coin denominations, and coins, needed to settle a transaction. Many US sporting stadiums round up prices to the nearest quarter dollar, but the discussion pointed out that for those on a very low income, every cent counts.

Coinstar was clear that any thought of rounding up needs to be done carefully both for this reason and because of the potential impact on circulation volumes.

Jim described the low value coins as ‘the sediment at the bottom of the tank’. Take away the penny and this creates inefficiency and lowers volumes. The low value coins spur redemption and create volume which makes the system work. Inflation though, can create a tipping point of inefficiency.

Cash crisis?

David suggested that when the cost of manufacture is greater than the face value, when more cash is coming in than is going out and when stock levels grow so large that they can’t be easily accommodated, then the cash and the cash system faces a crisis.

The panellists were challenged about whether there was a need to campaign for cash. It was suggested that financial inclusion is a huge issue, not dissimilar to climate change. Financial literacy is a major challenge and society needs to be clear on the benefits and role of cash.

The Federal Reserve does not believe there is an ‘access to cash’ problem in the US currently and it remains a major payment instrument. Its role is to ensure cash demand is met and to work for equitable access. It supplies cash to the public through intermediaries – the financial institutions – rather than directly. It was noted that large financial institutions have been taking out infrastructure, relying instead on retailers. Given lockdowns, this is one of the reasons for the coin circulation problem the US has experienced.

There has been so much change that it is hard to know what real change has happened. There have been coin demand ‘dampeners’, such as increased unemployment and stimulus payments made in electronic money, but it is hard to spot the trend.

Coinstar made the point that the pandemic is not over yet. Sadly, its impact is likely to last at least another year and we should all prepare for further swings in demand and supply, although probably not as great as those of 2020.

Ultimately what happens to cash is a political decision. The US is a market driven society, and the point was made that to date the US has been better at adding payment mechanisms than taking them away.

Subscriber content

Read the full article

Full access to Coin & Mint News articles, newsletters and archives.